Key Points

- Australia has significant geothermal resources; however, there are also significant challenges to exploiting these resources to produce energy or useable heat.

- While Australia saw a boom in activity and investment for geothermal resource development in the late 2000s, the industry has since faced several key challenges which have been financially damaging to some of the companies involved.

- Rapid and ongoing technology development in other renewable energy sources has also put the comparative benefits of geothermal energy under development pressure.

- Despite the challenges, there is still potential for improving Australia’s energy security with a viable geothermal energy source. This will require pragmatic and consistent research and development, which would represent a departure from the previous ‘boom and bust’ nature of the industry (as is common in other resource or energy industries).

Summary

There is huge potential for the extraction of geothermal energy in Australia. Geothermal resources in countries like New Zealand or Iceland are more easily used for electricity generation, since there is an abundance of pressurised hot water underground due to volcanic activity. In Australia, however, most geothermal energy needs to be extracted by pumping water from the surface through rocks deep below ground to absorb heat, and then circulating this water back to surface. Such a process is known as an Enhanced, or Engineered, Geothermal System (EGS). Following nearly ten years of promise and investor activity, the geothermal industry in Australia peaked in 2010, and to the end of 2013 saw a cumulative investment of around $900 million. Since then, and despite a successful power plant test in central Australia, investor and government sentiment towards the future viability of the industry as a power generation source seems to have waned significantly. Currently, the only ongoing project related to geothermal energy is a study of geothermal reservoir characterisation led by the South Australian Centre for Geothermal Energy Research at the University of Adelaide. This project is partly funded by the Australian Renewable Energy Agency (ARENA).

There are several reasons for the reduction in industry development progress. These can be grouped as: economic, technical, geographic, financial and policy-related challenges. Given ambitious plans for industrial and population growth in northern Australia, it makes sense that a potential source of baseload, renewable energy that is geographically close (and hence may not require significant amounts of transmission infrastructure) should continue to be seriously considered as part of a suite of energy security options. There is a future for a geothermal industry in Australia, but any development of the industry depends on how these challenges are met.

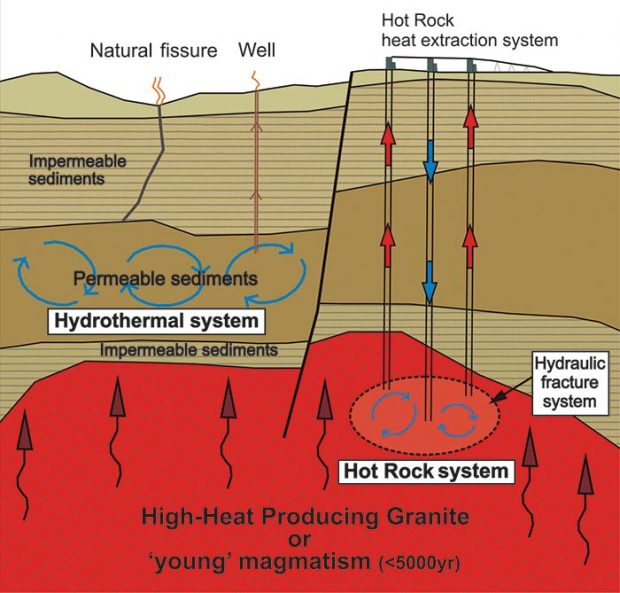

Figure 1: Geological settings of hydrothermal and hot rock geothermal systems in Australia. Source: Geoscience Australia.

Analysis

Introduction

In October 2013, publicly listed geothermal energy development company Geodynamics announced a successful 160-day trial of a 1MWe (Megawatts of electricity) pilot plant in the Habanero field, near the border between South Australia and Queensland. The pilot plant used steam generated through an EGS that exploits thermal energy from hot rocks over four kilometres below ground level. Following the trial, it was concluded that it may be economically viable to supply heat energy to nearby gas production operations, but not the supply of electrical energy. No further work has been done on the project, and the company completed site environmental remediation works in 2016. Given the success in proving the generation of electricity from geothermal resources, but the failure of the test to garner any significant momentum as an alternative source of energy, what might the future of the industry hold for Australia?

Economic challenges

A 2014 report for ARENA forecast a Levelised Cost Of Electricity (LCOE) range for power from EGS in 2030 that was favourable to coal or gas generation if there was a cost of carbon applied – and more so if Carbon Capture and Storage (CCS) technology was used. This LCOE was based on big reductions in project set-up and operational costs, and improved efficiencies in the generation of electricity from EGS projects. A 2016 report on power generation in Australia compared forecast costs between renewable and non-renewable electricity generation technologies, but did not consider electricity generated from an EGS source. The report did state that the maintenance of geothermal expertise in Australia is critical – which will be difficult given the lack of support for industry from market-based or government investment and a resulting flow of talent from Australia. The LCOE of wind or solar-generated electricity is also forecast to drop significantly by 2030, and given ongoing development of storage technology, geothermal energy may lose its relatively unique advantage of being both renewable and capable of reliable base-load generation.

Technical challenges

EGS (also described as a hot rock system) extracts heat from hot rocks deep in the earth and conveys it to surface where it is used to generate electricity (see Figure 1 above). This involves a heat exchange arrangement. In most EGS projects, water is pumped into an injection well where it takes on heat as it moves through fractures in hot rock, and is then extracted to surface from a production well. In the Habanero pilot plant trial, temperatures seen on surface from the production well were up to 215 degrees by the time the trial was finished – certainly demonstrating the capacity to extract heat. Another critical factor in how much electricity can be generated though is the rate at which the high temperature steam is produced. In the Habanero trial, up to 19 kg/s of flow could be sustained. This contrasts with (according to the 2014 report to ARENA) flow rates in the order of 80 to 100 kg/s that would be required for economic viability. Whereas the initial intention of the Habanero project was to create a network of man-made fractures to allow optimal rates of circulation, in actuality, fluid was circulated through a naturally occurring fault in the rock (a geological feature which was not anticipated). The challenge of establishing and optimising fluid circulation between wells might be addressed in future through fracturing techniques that have resulted from ongoing technology development in tight gas or oil wells.

It must be noted that geothermal resource development is a very different application from unconventional oil or gas development, and there is much more separation between EGS reservoirs and existing groundwater sources. Application, however, of similar technologies has proven to be politically and socially controversial and are likely to continue to be so.

Geographic challenges

A further challenge to the industry is the separation between potential geothermal resources and existing or planned population centres in Australia. A heat distribution map for Australia at 5km depth shows that while there are large potential resources for heat extraction, these tend to be distant from most capital cities. The cost to transmit power from a potential large-scale power plant at the Habanero site to eastern New South Wales was estimated at up to $843 million – which is not much less than the total investment made in the geothermal industry up to the end of 2013. Even if geothermal resources may not be appropriate for powering existing major population centres in Australia, there is still potential for the supply of energy to regional industries (like the offshore oil and gas operations in the north-west of Australia, or onshore operations in Queensland) and to fuel the development of areas which don’t already have established power grids.

Financial challenges

The ability of the industry to attract sufficient investment to ensure initial development and construction costs has, and will continue to be, challenging. The amount of time between concept and commissioning for a geothermal project is generally not attractive to many investors. Since launching on the Australian Stock Exchange, Geodynamics took around 10 years to prove that electricity could be generated from its Habanero pilot plant. The wells drilled were amongst the most technically challenging in Australia due to extreme temperatures and pressures seen at depth, with numerous unwanted events such as mechanically or chemically induced equipment failures. While these technical challenges did contribute significantly to international industry knowledge, they also resulted in very high costs and the alienation of investors.

In another example, Petratherm, a listed company with plans to generate electricity from a geothermal resource in South Australia, drilled the first of a two-well set in 2009, and announced water flow test results in 2011. This company, however, lost access to a $13 million grant from ARENA to drill a second well in 2014, because it was unable to secure additional equity from non-government sources – despite already having an established oil and gas sector operator as a joint venture partner who had committed partial funding of the well.

Policy challenges

Australia has a long and inconsistent history of climate change policy. Most notably, in the years between 2007 and 2015, several initiatives to reduce and mitigate climate change were introduced, modified, and subsequently scrapped. The political fallout was significant, as was evident by the contribution it made to a change of government during that time. This inconsistency in policy has also meant that there has been, and will most likely continue to be, uncertainty surrounding the financial viability of geothermal energy. Many LCOE comparisons between renewable and non-renewable energy sources include variability on costings due to a potential carbon price or possible requirement for CCS for fossil fuels. Without any certainty on whether either, or both, of these aspects will affect the Australian energy generation market, investors will not be forthcoming with capital to support technology development.

Conclusion

The geothermal industry in Australia has shown significant innovation in its activity. While it has not been able to demonstrate economical large-scale power generation so far, it has shown sufficient potential for geothermal technology to be included in a suite of options to ensure Australia’s future energy security, and, as such, should be pursued with ongoing investment in research and development.

August 29, 2017

John Macfarlane, Research Analyst, Northern Australia and Land Care Research Programme

Published by Future Directions International Pty Ltd.

-

By: Future Direction International

Future Directions International (FDI) is an independent, not-for-profit Research Institute. It was established in 2000, by Major General (Retd) the Honourable Michael Jeffery (former Governor General of Australia) together with a small group of leading Australians, to conduct comprehensive research of important medium to long-term issues facing Australia.

I personally ask you to consider a donation to FDI which will allow the institute to continue research of vital importance to Australia and future generations of Australians.

-